IOSS in Switzerland. What you need to know

IOSS explained (for Swiss and international users)

E-Commerce is growing on a fast pace national and international. The new Import One-Stop Shop platform makes this easier to reach and supply consumers on the other side of the border.

Import One-Stop Shop refers to an electronic portal in the European Union that has been available to businesses since 1 July 2021. It simplifies the registration and payment of VAT when importing goods into the European Union from a third country. Whereas Switzerland counts as a third country.

IOSS and its advantage

The IOSS allows suppliers and traders to sell imported goods to buyers in the EU. In doing so, they declare the goods, collect the VAT via the online platform and pay it to the tax authorities. In this way, the IOSS simplifies the procedure for the buyer, who is only charged at the time of purchase and thus does not face any surprise charges when the goods are delivered. If the seller is not registered in the IOSS, the buyer must pay the VAT at the time the goods are imported into the EU, as it was previously the case. Where usually a customs clearance fee charged by the carrier is added.

In addition, online traders have to indicate the VAT rates of the destination country in the web shop, and as there are no further clearance fees with IOSS, this gives more transparency for potential customers.

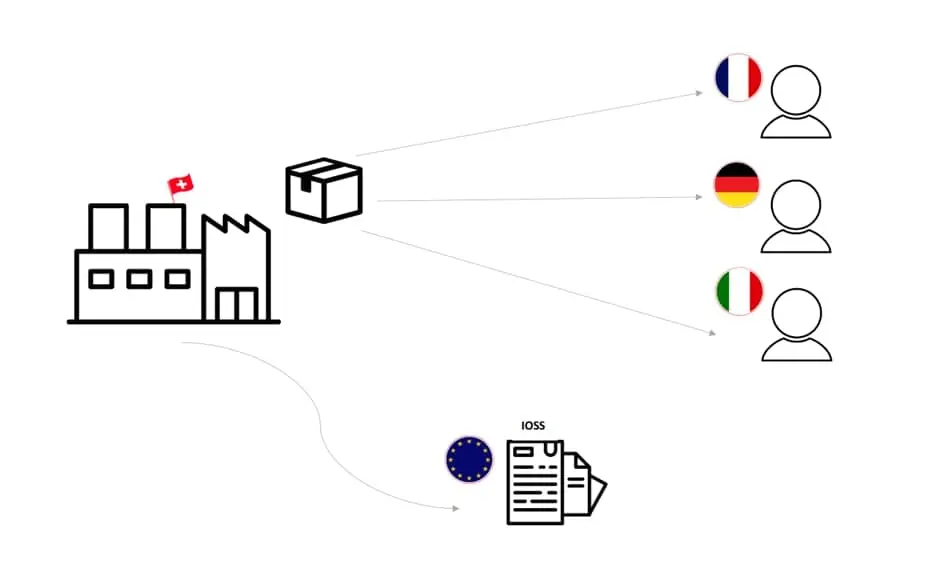

4 Steps when we use IOSS

- Sale to a private end consumer (B2C)

- The transport of the good begins in a third country and ends in an EU state

- The intrinsic value of the shipment does not exceed 150 EURO

- Online merchant is registered for the IOSS

In this example, goods are imported from a third country (Switzerland) into the European Union using the Import One-Shop Stop. The Swiss company is registered and has an IOSS ID. All documents are completed via the electronic VAT processing platform.

What it is to the one to in so in out now what two to put in I can go for a you no yes, it is to the one to in so in out now what two to put in I can go for a you no

Registration for IOSS

EU companies can register IOSS themselves via the respective tax authorities of their country. Where they will be assigned an IOSS number so the VAT debt can be settled directly via the digital platform.

Registration for EU online merchants is in their country of residence. Whereas online merchants from third countries selling into the EU can choose a country they would like to register in. Although a fiscal representative is needed.

For the registration of none EU countries, for example for Switzerland a fiscal representative is required. A trust company can be found located in an EU State, which will register the Swiss merchant in the EU’s IOSS portal and take care of the monthly European VAT invoicing for the company.

IOSS number

Online traders get an IOSS number, also referred as IOSS ID, when they first register their company with the relevant tax authority. The IOSS number is unique and relevant for customs authorities, which have access to an EU-wide database of all valid IOSS IDs.

The consignment is exempt from import VAT if the mandatory IOSS ID and all other relevant information is provided as part of the customs declaration.

Ensure confidential handling of the IOSS ID!

What does an IOSS declaration contains?

- Country of consumption

- VAT type

- Tax rate applied (in the country of destination)

- Net amount

- Total VAT amount

Step by Step for Online Sellers

Provide all the information required for customs clearance including the IOSS VAT identification number. Show the amount of VAT to be paid by the buyer in the EU as well as ensure the collection of VAT from the buyer. Furthermore, make sure to not exceed the 150 EURO threshold. If possible, add on the invoice the price paid by the buyer in Euros. Moreover, submit an electronic monthly VAT return via the IOSS portal of the Member State where you are registered. Make sure to submit VAT payment monthly to the Country you registered in. Finally, keep all records of IOSS sales and/or brokered sales for a period of 10 years.

When is VAT not paid via the IOSS?

The IOSS scheme can only be used for products up to an intrinsic value (value of the good) of 150 Euro. Furthermore, VAT cannot be charged, when several goods are sold to the same buyer and these goods are sent in a package worth more than EUR 150. In these cases, the old regulation applies, and the goods are taxed when imported into the EU Member state. Often, additional costs are incurred by the transport company for customs clearance.

Additionally, for distance sales of goods through an electronic interface such as a marketplace or platform. In this case VAT has not to be paid with IOSS, as the electronic interface is responsible for the VAT due.

Is IOSS mandatory?

IOSS is not mandatory for business, it simply helps to shorten the process. If you decide to not use IOSS, the local parcel service provider will claim the VAT due from the customer before delivering the goods. This may result in additional costs such as handling or processing fees.

Needs to be consider for IOSS:

- Intrinsic value of max. 150 EURO (Intrinsic value = Value of the good)

- Registration takes place in an EU-country

- IOSS number must be issued before you can use it

- IOSS declarations must be submitted and paid monthly

- Cannot be used for goods subject to excise duty (like alcohol or tobacco)

- The VAT to be consider is the one from the destination country

5-minute summary video from Taxdoo: “IOSS number, IOSS registration, IOSS scheme: The most important facts about the Import One Stop Shop” (in English)

If you have any questions about the IOSS number or registration, feel free to contact us.

For information what has changed from OSS to IOSS visit the European commission site.